This article reports the actual results of personal brokerage accounts owned and managed by SignalStrike’s founders for the period stated, using the SignalStrike platform with self-selected parameters. These are personal-account results — not the performance of any fund or pooled investment vehicle, not shown net of any fund fees, and not independently verified by a third party. They are not investment advice, not a solicitation, and not representative of any other investor’s outcome; another person’s results will differ, potentially materially, with their own parameters, timing, and market conditions. Past performance is not indicative of future results, and momentum strategies have historically suffered severe drawdowns — see Momentum Crashes. See the full disclosures at the end of this article.

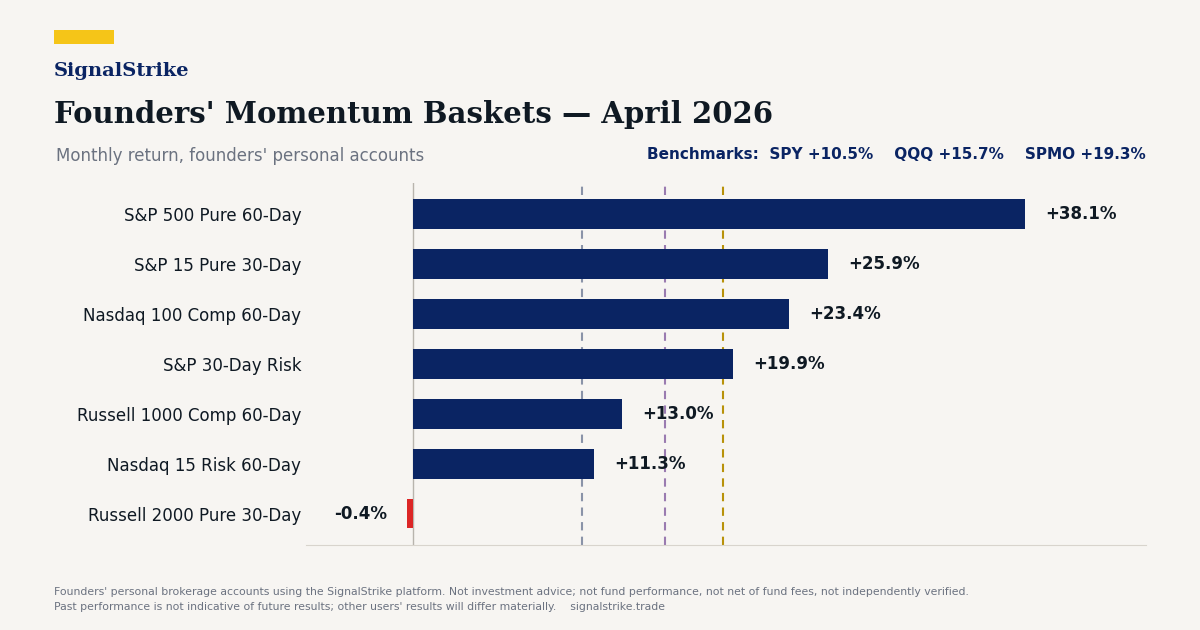

April 2026 was a sharp recovery month. Benchmarks rebounded hard, led by large-cap growth and passive momentum. Most of the founders’ baskets captured the rebound and several led their benchmarks — but the cash protection that helped in March cut the other way for one basket that re-entered late and finished roughly flat while small-caps ripped higher. Timing risk runs in both directions.

The short version. Benchmarks rebounded sharply — SPY +10.51%, QQQ +15.69%, SPMO +19.34%. Most founders’ baskets captured the recovery, several led, and one that re-entered late finished roughly flat. A two-month rebound is not a normal run rate and should not be extrapolated.

April 2026 in market context

April reversed March hard. SPY rebounded +10.51%, QQQ +15.69%, and SPMO +19.34% — with passive momentum leading the recovery. Small-caps also rallied sharply. The speed of the reversal is exactly the condition that punishes defensive positioning held too long.

Founders’ baskets — April 2026 results

Returns below are calendar-month figures for April 2026. Each basket column is the change in the founders’ actual end-of-day brokerage account balance; the SPY, QQQ, and SPMO columns are the same-month total returns (dividend-reinvested) for those ETFs.

| Basket | April 2026 | SPY | QQQ | SPMO |

|---|---|---|---|---|

| SP500 Pure 60-Day | +38.15% | +10.51% | +15.69% | +19.34% |

| NASDAQ 100 Composite 60-Day | +23.43% | +10.51% | +15.69% | +19.34% |

| Russell 1000 Composite 60-Day | +13.01% | +10.51% | +15.69% | +19.34% |

| NASDAQ 15 Pure Risk 60-Day | +11.29% | +10.51% | +15.69% | +19.34% |

| S&P 30-Day Pure Risk | +19.94% | +10.51% | +15.69% | +19.34% |

| Russell 2000 Pure 30-Day | -0.38% | +10.51% | +15.69% | +19.34% |

| S&P 15 Pure 30-Day | +25.86% | +10.51% | +15.69% | +19.34% |

Source: founders’ brokerage balances via signalstrike-portfolio.vercel.app; benchmark closes via Tiingo (dividend-reinvested). All seven baskets are individual brokerage accounts held by the founders.

⚠️ Performance disclosure. Returns shown reflect SignalStrike founders’ personal brokerage accounts for the stated period, achieved using the platform with self-selected parameters. They are personal-account results — not the performance of any fund, not net of any management or performance fees a fund would charge, and not independently verified by a third party. Any other user’s results will differ, potentially materially, based on their own parameters, entry and exit timing, and market conditions. Past performance is not indicative of future results. All investing involves risk, including the loss of principal.

What happened — abstracted commentary

April was about re-engaging risk after March’s defensive moves.

NASDAQ 100 Composite 60-Day re-entered from cash early in the month, shifting to an equal-weight construction at re-entry, and captured much of the rebound.

Russell 2000 Pure 30-Day re-entered later in the month after holding its defensive position — and that delay is visible in the numbers: it finished roughly flat while small-caps rallied sharply. The same cash protection that helped in March hurt here. This is the clearest example in the series of timing risk cutting against the strategy.

NASDAQ 15 Pure Risk 60-Day made a discretionary selection-mode change (from pure momentum to a momentum-plus-market-cap construction) and trailed its large-cap-growth benchmark for the month.

SP500 Pure 60-Day and S&P 15 Pure 30-Day ran their scheduled rebalances and led the field.

Methodology

- Basket returns are the calendar-month change in the founders’ actual end-of-day brokerage account balances, read from the public tracker at signalstrike-portfolio.vercel.app. Each monthly figure is the percentage change from the prior month-end balance to the current month-end balance, and the monthly figures chain exactly to each basket’s since-inception return.

- Benchmark returns (SPY, QQQ, SPMO) are calendar-month total returns computed from Tiingo adjusted-close prices, which incorporate dividend reinvestment.

- Benchmarks are references, not style-matched indices. SPY (broad market), QQQ (large-cap growth), and SPMO (Invesco S&P 500 Momentum ETF, a passive momentum implementation) are shown for every basket for consistency — they are not each basket’s underlying universe.

- No deposits or withdrawals occurred in any existing basket during the reporting months, so monthly account-balance changes equal monthly returns directly. The S&P 15 Pure 30-Day basket was funded once at inception (January 21, 2026).

- Dividends. Basket figures are actual broker account balances, which include any dividends received as cash; benchmark figures use dividend-reinvested adjusted-close prices. Both sides are therefore on a total-return basis.

- Holdings are never disclosed. Per SignalStrike’s content policy, the strategy commentary in this article describes rebalance types and mechanics only — never individual position names.

Frequently Asked Questions

Are these returns from real accounts or backtests?

They are from real brokerage accounts owned by SignalStrike’s founders. Each basket runs in a separate live account at Schwab or E*TRADE, and the figures are end-of-day account balances — not simulated or backtested results.

Are these returns representative of what a SignalStrike user would experience?

No. These are the founders’ personal accounts. A user’s results depend on their own strategy configuration, account size, brokerage, rebalance and execution timing, and tax situation. SignalStrike users build their own strategies with their own parameters; the founders’ baskets are not a model portfolio to replicate.

Why is SPMO included as a benchmark?

SPMO is the Invesco S&P 500 Momentum ETF — the most direct passive momentum comparison available. Beating the broad market (SPY) and beating a passive momentum implementation (SPMO) are different claims, so SPMO is included as the harder, more relevant benchmark for a momentum strategy.

What are the risks of these strategies?

Momentum strategies are vulnerable to severe, rapid drawdowns — especially during sharp reversals after extended trends, a pattern known as a “momentum crash.” Daniel and Moskowitz (2016) documented historical momentum drawdowns exceeding 70%. See Momentum Crashes.

Why did one basket stay roughly flat while the market rallied in April?

The Russell 2000 Pure 30-Day basket held a defensive cash position into April and re-entered later in the month, missing much of the early-April rally. Defensive positioning protects in selloffs but creates the risk of re-entering late into a sharp recovery — a real cost that April made visible.

Further Reading

- Momentum Investing: How It Works and Why It Persists — the strategy these baskets implement.

- Momentum Crashes: The Hidden Risk in Momentum Investing — the well-documented failure mode, with Daniel & Moskowitz (2016).

- Risk-Managed Momentum: Scaling Exposure to Volatility — how risk management is applied at the ranking and portfolio layers.

- Public live tracker (updated daily): signalstrike-portfolio.vercel.app

Related Research

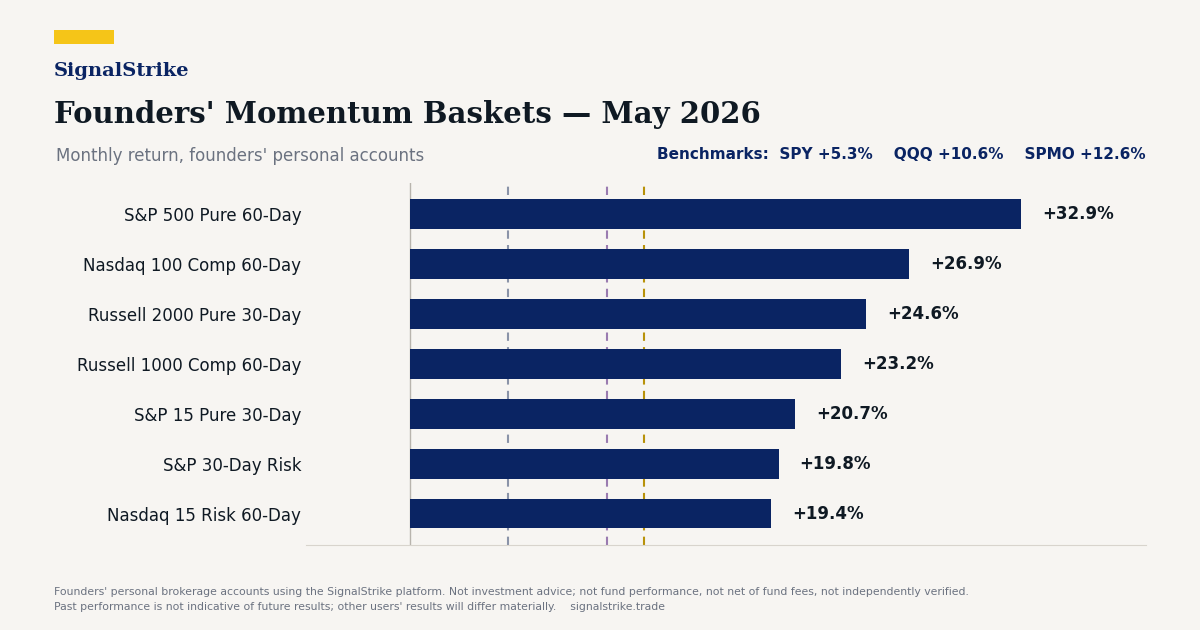

- Founders' Momentum Baskets: May 2026 Performance — How SignalStrike's founders' momentum baskets performed in May 2026 against the S&P 500, Nasdaq 100, and S&P 500 Momentum ETF, with full methodology.

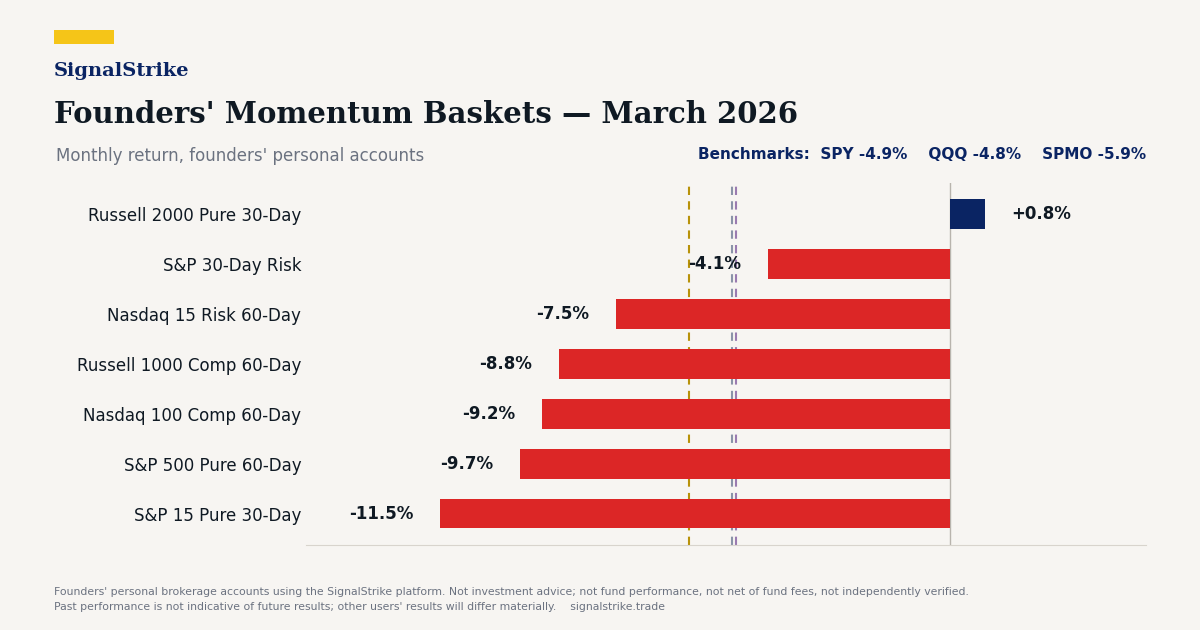

- Founders' Momentum Baskets: March 2026 Performance — How SignalStrike's founders' momentum baskets performed in March 2026 against the S&P 500, Nasdaq 100, and S&P 500 Momentum ETF, including drawdown risk.

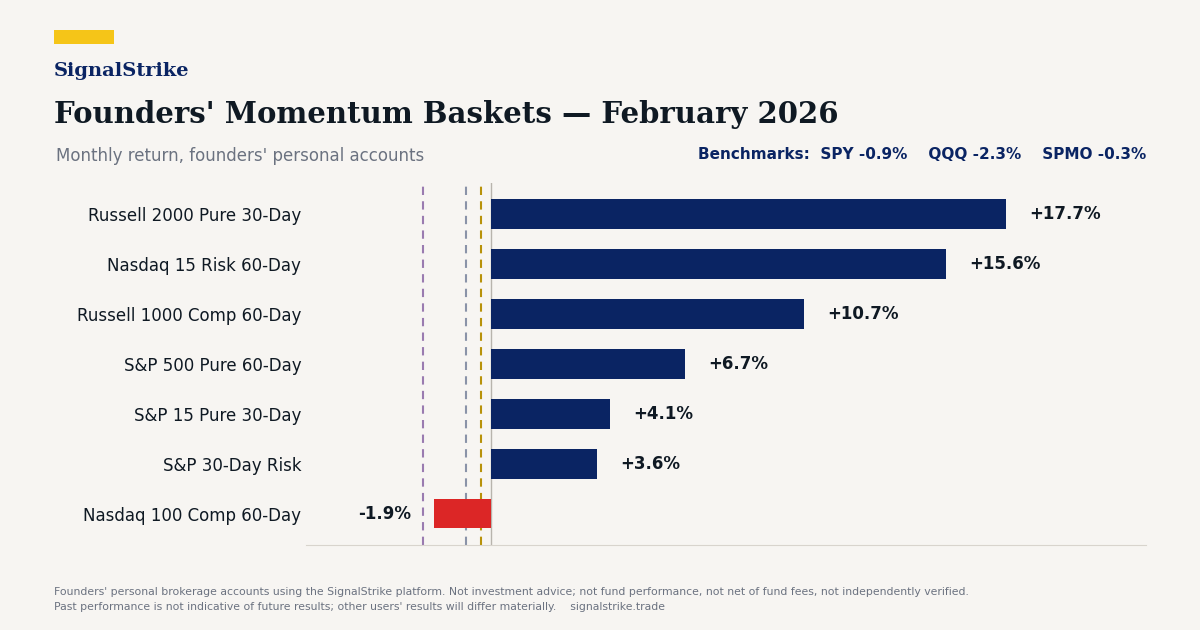

- Founders' Momentum Baskets: February 2026 Performance — How SignalStrike's founders' momentum baskets performed in February 2026 against the S&P 500, Nasdaq 100, and S&P 500 Momentum ETF, with full methodology.

Disclosures

SignalStrike is a software platform providing research, screening, and backtesting tools focused on U.S. equity momentum. It is not a registered investment advisor (RIA), does not provide personalized investment advice, and is not a broker-dealer.

The performance shown in this article reflects the actual end-of-day brokerage account balances of SignalStrike’s founders for the specific period stated, achieved using the SignalStrike platform with self-selected parameters. These are personal-account results. They are not the performance of any fund or pooled investment vehicle, are not presented net of any fund management or performance fees, and have not been independently verified or audited by a third party. They are not a model portfolio, are not representative of any other investor’s experience, and are not a projection or guarantee of future returns. Any other user’s results — whether using SignalStrike’s platform or otherwise — will differ, potentially materially, based on the parameters they select, account size, brokerage, fee and tax considerations, rebalance and execution timing, and discretionary decisions.

The founders applied discretionary overrides during the periods reported (for example, defensive rotations to cash, selection-mode changes, and manual position adjustments). These strategies are therefore rules-based with discretion, not fully mechanical.

Past performance is not indicative of future results. All investing involves risk, including the loss of principal. Momentum-based strategies have historically suffered severe and rapid drawdowns during specific market regimes; some reported months were favorable for the strategy and are not representative of all market conditions.

Benchmark performance for SPY (SPDR S&P 500 ETF Trust), QQQ (Invesco QQQ Trust), and SPMO (Invesco S&P 500 Momentum ETF) is calculated from Tiingo adjusted-close prices, which incorporate dividend reinvestment. Direct investment in an index is not possible; ETF returns may differ from the underlying index due to expenses and tracking error.

This article does not constitute an offer to sell, or a solicitation of an offer to buy, any security or investment product. SignalStrike does not custody funds or execute trades on behalf of users; users execute through their own brokerage accounts at their sole discretion.

Securities products and services referenced are offered through users’ own brokerage accounts under existing custodial relationships. Advisory firms evaluating any tool for use with client portfolios remain solely responsible for fiduciary, suitability, and disclosure obligations under applicable law.